Time to overweight listed real estate?

Time to overweight listed real estate?

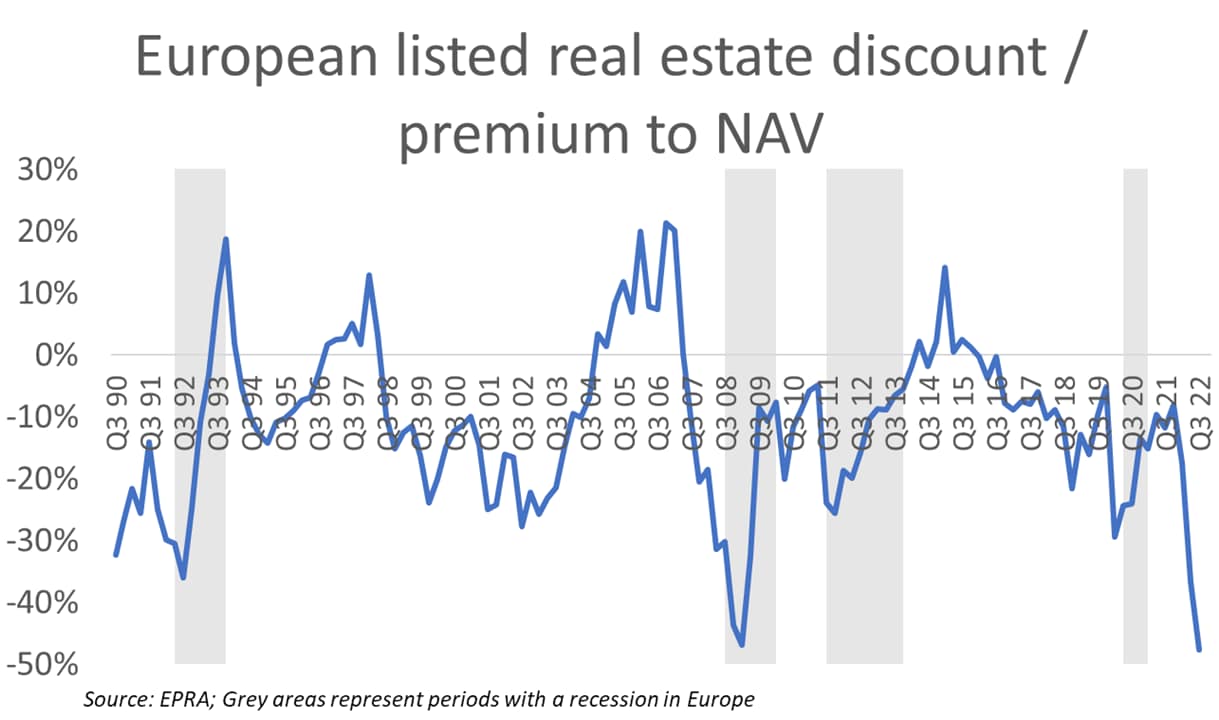

With the constant talk about inflation and recession, real estate performance is under pressure. Valuations are down as a result of soaring interest rates. Listed real estate performance has been very weak (-37%1) in 2022, which has led to a very significant discount to NAV, as presented in the graph below.

As shown, discounts are especially high at the start of each recession, reflecting the concerns investors have about the economy and the obvious negative impact on real estate. This discount is typically driven by a drop in share prices, while NAVs are still stable or even rising, caused by slow moving (lagging) valuations.

The interesting question is, however, what this discount/premium indicator tells us about future performance. So, whether we could use this measure to improve our investment performance and optimise our real estate portfolio. To test this, I compared the average discount rate with the next 5 years’ performance of listed and private real estate2. More specifically, I used the difference in return between listed and private real estate funds. As the compositions of both are really different, I adjusted the private real estate fund performance to match the sector composition of the listed market, creating an artificial private universe. One should, however, realise that some sector/market combinations are best or most widely available private and some public.

The results of the analysis are shown in the graph below. The graph only covers the period from 2004 onwards, as the data availability and quality is less in earlier years. Each dot in the chart represents the discount/premium at a certain quarter and the difference in return over the next 5 years, annualised. What is clear from this analysis, is that listed typically outperforms when there is a discount to NAV (top left quadrant), and it will underperform when there is a premium (bottom right quadrant). It also highlights that listed mostly trades at a discount. The red line represents the best fit relationship between the discount and relative return and it shows that the fit is strong (R2=0.57). It also highlights that private outperforms when the discount to NAV is zero.

Although this negative relationship is in line with expectation, it is valuable to have this confirmed by data. Moreover, the fitted line can help to make choices based on the current discount or premium. Let’s assume that today’s discount is 25%, this would imply that the listed market is expected to outperform with 7.5% per annum over the next 5 years. This difference could be sufficient for investors to shift part of their private real estate portfolio to public real estate, even when they need to accept some additional reduction of the current NAV of their private real estate exposure when selling. It also shows the importance of incorporating liquidity as part of your real estate portfolio construction to benefit from this opportunity.

A more in-depth paper covering the research in this blog is available upon request. For this paper or for more information about this research or about other topics, please visit www.spekadvisory.com.

1Source: EPRA Europe General Index

2Source: EPRA for public and INREV Fund Index for private real estate