How the investment horizon impacts risk profile

How the investment horizon impacts risk profile

Understanding private asset data is key in building the right allocation decisions

Ever had a discussion about whether listed real estate is equity or real estate? Or whether listed infrastructure is equity or infrastructure? These are fair questions to raise, but not easy to answer, as it depends…It depends on what you are trying to solve.

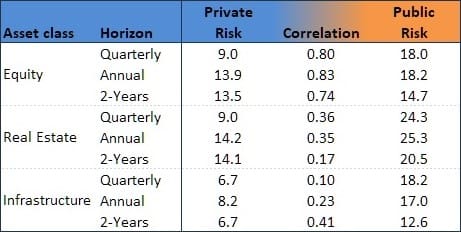

One of the most important factors in this debate is the assumed investment horizon. On a liquidity basis, private and the public equivalents are clearly different. But let’s look at this issue from an allocation point of view. A typical allocation model needs assumptions on risk and correlation, which is normally estimated using historical data. When using quarterly data, we can observe quite a difference in risk between public and private markets, as shown in the table below.

Table 1: Risk (standard deviation in %) of and correlation between private assets and public equivalents, from 2008 – Q3 2022. Source: Preqin Ltd, Russel, MSCI and S&P, modified by Spek Advisory

Private markets are typically showing a risk that is only half or even a third of the public market equivalent, while public real estate and infrastructure risks are more in line with public equity. A lot can be said about the quality of the data and the fact that the private data is valuation based, but nevertheless this quarterly based gap is the main reason why public equivalents can be seen as equity.

For allocation purposes, one needs to consider the investment horizon of the investor. Everybody knows that this horizon is much longer than one quarter. So if the horizon is longer, why are we just looking at quarterly relationships? Why aren’t we looking at longer term relationships? An additional benefit of expanding the time frame we use for the analysis, is that things like market sentiment or valuation smoothing will have a lesser impact. The results for a 2 year horizon are also shown in table 1. And yes, I know – 2 years is still lower than the typical investment horizon. However, this 2 year time frame already captures the relevant conversion. As shown in the table, risks of public and private assets are actually converting. Private risks are rising, while public risks are falling. Also correlations seem to be increasing due to the longer time frame used.

All these observations are based on data from Preqin, which are typically more biased towards the US and the more opportunistic segment of the market. In addition, I did not adjust the data to create a like-for-like basis. Using more suitable data and making the appropriate adjustments, however, differences are even smaller between public and private assets.

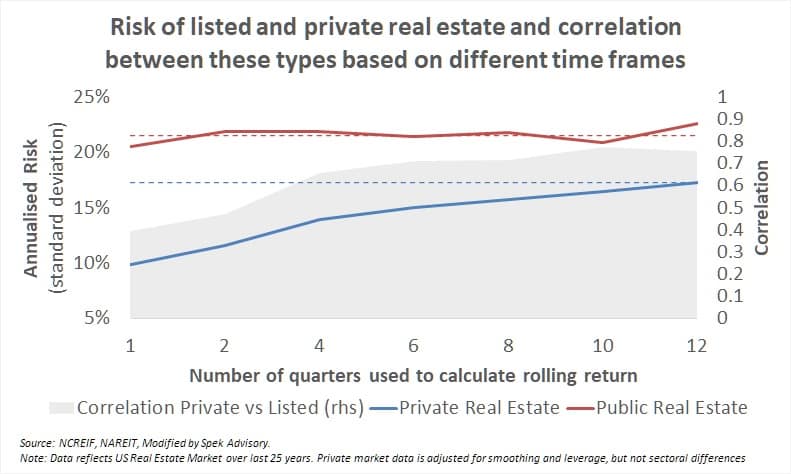

For instance, look at the real estate risks and correlation in the above graph. On a quarterly basis the correlation is only around 0.4, while it consistently increases when extending the time frame until it doubles when approaching 3 years. Private real estate risk was half of the public equivalent, but increases to 80% after 3 years. Although the data could be even further refined by adjusting for sectoral differences, the conclusion is rather clear: based on longer investment horizons, private real estate is very similar to public real estate and vice versa. And with the right data, the same is true for infrastructure. Private equity is a slightly different case, as it is driven by higher return targets. Nevertheless, using a longer term investment horizonwill provide a better risk profile of the asset class.

More in-depth analysis covering the research in this blog is available upon request. For more information about this research or about other topics, please contact us.