The impact of higher rates on real estate

The impact of higher rates on real estate

Higher rates lead to a repricing of risk, with more income driven portfolios benefiting.

Low interest rates are typically good for growth companies, as values in the distant future are discounted at low rates. Higher rates, like we see today, are better for value stocks, where value is more income driven. This same analogy can be used for real estate. A lack of income, due to vacancy, active management, high leverage or (re)development does not seem to be a huge risk when rates are low, but start to become a bigger risk when rates are normalising. Values will be impacted and investors should position themselves accordingly.

To fight inflation, Central Banks raised policy rates sharply and as a result, US and European yield curves are now inverted, which is known to be the best indicator for an upcoming recession. These high rates, however, broke something along the way: a number of banks. Are we now entering a new financial crisis? That is still to be seen, but what higher rates do, is getting rid of excesses. More companies are likely to follow, as some companies are just not efficient and profitable enough to sustain these higher rates. The impact on private asset fundamentals could remain limited, as long as the unemployment rate stays low. If unemployment surges, a downturn for private assets can be expected as well.

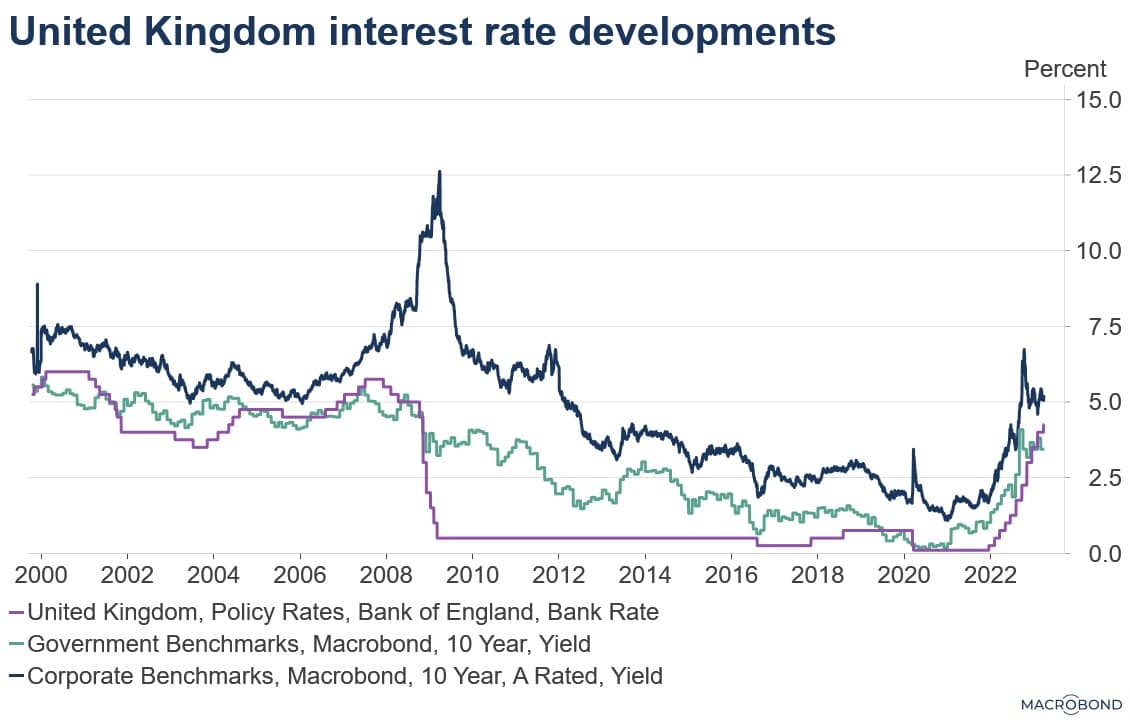

Interestingly, these bank failures have led to a turning point in rates, with yields expected to stabilise or even decline. Will this help real estate yields to stabilise? Well, yes and no. Although policy rates are expected to decline, risk spreads might rise further due to new bankruptcies, increased uncertainty and a potential recession. All of these will be very bad for private asset loans, especially for the more risky assets. Refinancing real estate debt will be more challenging in the coming years. The cost of finance has doubled already (see first graph, where UK rates were around 2.5% in ‘16-‘18, while they are around 5% today, with the corporate A-rated bond as a proxy for real estate rates). And as valuations are lower today, funds and investors likely need to bring more equity and accept less favourable conditions when refinancing.There will be, however, a repricing of risks due to more normalised rates.

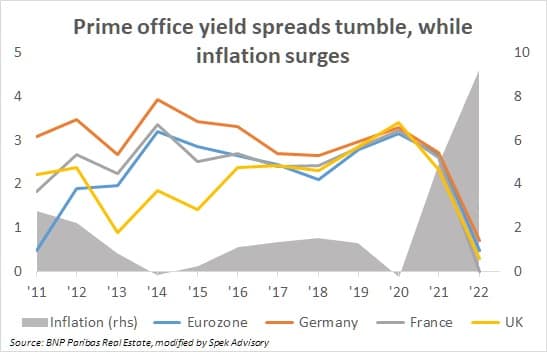

In the graph above, yield spreads are shown for prime offices in several countries versus European inflation. Currently, spreads are very low, just above 0, which is only possible due to strong rental growth driven by inflation. As soon as this rental growth is fading, due to a decline in inflation or a recession, spreads will rise. There are, however, also a number of asset specific reasons for weak rental growth, such as poor asset quality or location, weak sustainability and quality of management.

So how should investors position themselves in this environment? Well, some risks are just not worth taking. In this environment, income is appreciated upwards, while growth should be valued less. Try to proactively reduce that part of the portfolio where the risk of a loss of rental income is the highest. Moreover, make sure to have some liquidity available to benefit from distress in the market, which is likely to happen.

Some risks are not worth taking. This concept will come back in later blogs, when each of these risks will be highlighted and discussed in more detail. If you want to know more, or if you are interested in other research and strategy topics, please contact us.