Retail is back

Retail is back

Investors should seriously consider to embrace retail as part of their allocation again

Since 2016, the retail sector has been underperforming the overall market. Investors decreased their allocation and sold their retail assets accordingly. As a result, repricing has been substantial. However, there are now indications that retail has started recovering. It is time for investors to increase their allocation again.

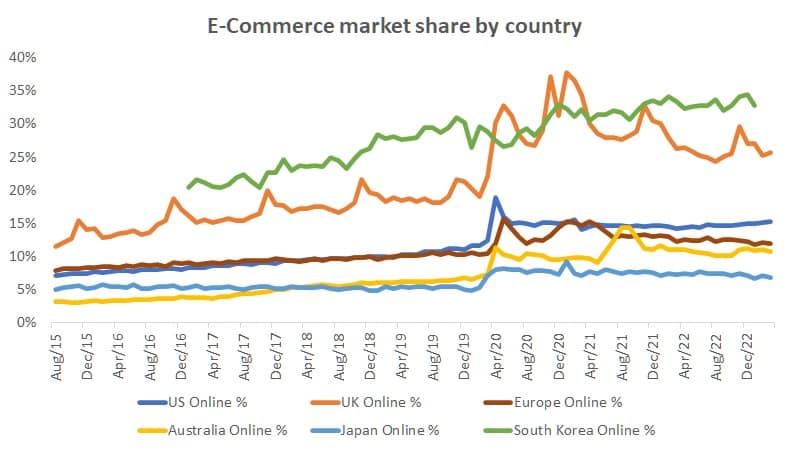

Online retail sales have been growing strongly since 2016. The Covid-19 pandemic accelerated these numbers, leading to a peak in online sales. The highest penetration levels were seen in South Korea and the UK with levels above 30%, while the US and Europe reached levels of 15%.

Figure 1: E-commerce market share as % of total retail sales for a number of countries. Source: Macrobond, modified by Spek Advisory

Since 2020, however, penetration levels have more or less plateaued, with some markets even showing some decline (mostly UK and Europe). I am not suggesting that these penetration rates have peaked entirely, but what this means is that growth rates will be less destructive for offline (in-store) retail going forward.

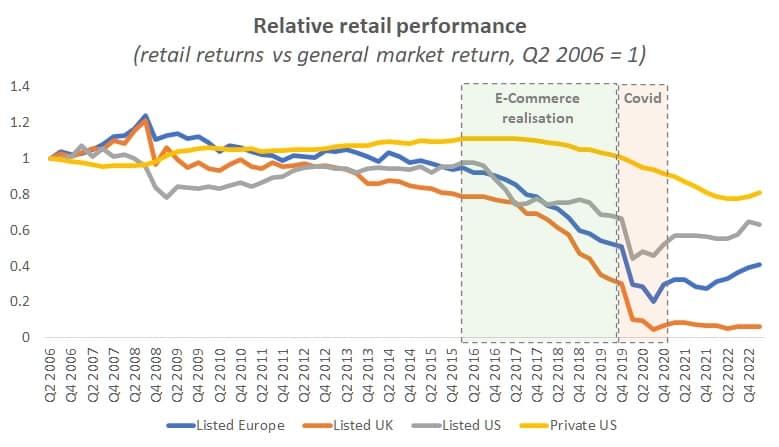

A great example is the UK, where online market share peaked above 35% during Covid-19. This had a massive impact in the repricing of retail real estate, as shown in figure 2. UK retail was the worst hit retail market globally and hasn’t really shown a recovery yet. Although the universe behind the index is limited, similar conclusions can be drawn using private indices. The retail markets in Europe and the US, on the other hand, are showing clear recovery compared to the overall market.

Figure 2: Underperformance of retail vs. entire market for listed real estate in Europe, UK and US and private real estate in US. Relative performance is measured as retail index divided by market index. Source: EPRA/NAREIT, NCREIF, modified by Spek Advisory

Retail underperformance has been structural for a number of years. However, since the acceleration due to Covid-19, retail has started to display outperformance. Due to the peak in inflation, rates started to rise and real estate has repriced as a result. As retail already experienced a repricing due to structural reasons, it has not seen much decline in value1. Given the level of repricing since 2016, the current relatively high yield, stabilization of online penetration and growth offline retail sales, investors should seriously consider investing in retail again.

Although I think it is the right time to increase the allocation, retail will not be without any obstacles. Managing a retail portfolio is much more complicated today than it was before e-commerce. Expert management and strong asset selection skills are a must. Yields are now much higher, but costs equally so, as is the structural vacancy. Also, the total return will be more income driven and less driven by value growth. Nevertheless, today’s pricing should provide a great opportunity to lock in great assets and long term returns.

If you want to know more about how to optimize your real estate portfolio, or if you are interested in this or other research and strategy topics, please contact us.

1 See for instance Green Street Pan-European CPPI: Sector-Level Indexes. Retail shows a -5% value decline vs. -20% value decline for the core sector average