The appeal of real estate debt

The appeal of real estate debt

High interest rates & low real estate spreads: an ideal moment to invest in real estate debt

In times when interest rates are moving materially, I expect real estate debt to be in the news a lot. Refinancing will be tough and expensive. Leverage ratios have increased, but need to come down again. However, for investors on the other side of the capital stack, these periods offer ample opportunities. There isn’t much research available on the risk return profile of real estate debt. I analysed this in my academic paper “Investing in real estate debt: is it real estate or fixed income?”1. I will use this paper to explain how real estate debt is positioned in today’s investment environment.

The use of debt is fundamental to the real estate industry. An example of a simple capital stack is shown in the chart below. The bar on the right shows the real estate investment and the bar on the left demonstrates a financing structure using 2 types of finance: senior & mezzanine. The senior tranche takes priority over all others and is typically a fixed interest rate. Mezzanine is subordinate to the senior tranche, but senior to the real estate equity. As a result, mezzanine is less secure than senior, but more secure than the equity holder.

Figure 1: Typical real estate capital stack when using mezzanine

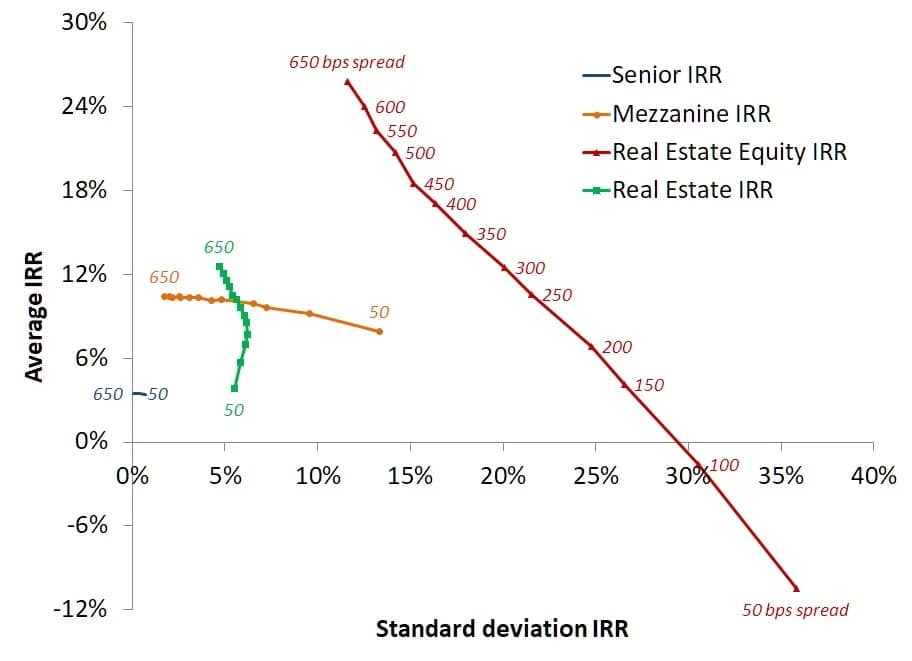

Interestingly, there is not much literature on how the risk return profile of mezzanine relates to that of real estate or senior debt. Based on some logical assumptions, it is however possible to create a cash-flow model that describes a real estate investment with a senior and mezzanine tranche. It gets interesting when this cash-flow model is tested with thousands of different market scenarios. As a result, it is possible to calculate the risk and return for each part of the capital stack. Moreover, it is possible to test for different levels of real estate yield spreads (difference between real estate yield and senior debt rate). The results for a 60% senior, 10% mezzanine and 30% equity capital structure are shown below.

Figure 2: Risk vs 5-year average IRR of each part of capital stack (60% senior, 10% mezzanine and 10% real estate equity) for different levels of real estate yield spread and relative to underlying real estate

Figure 2: Risk vs 5-year average IRR of each part of capital stack (60% senior, 10% mezzanine and 10% real estate equity) for different levels of real estate yield spread and relative to underlying real estate

As the chart shows, senior debt is like fixed income with a low 5-year average IRR and not much volatility. Real estate equity (70% levered) is very volatile and doesn’t show strong results when spreads are below 300 bps. Mezzanine, on the other hand, shows very strong returns, almost independent from the level of spread. Returns and risks are more in line with the underlying real estate portfolio and stay elevated when spreads are low.

So what does this tell us about the current situation? Rates and risk premiums have surged and spreads remain low, as yields have moved out. At current spreads, mezzanine is most likely to show the best next 5-year IRR, relative to real estate, senior debt or real estate equity. Moreover, given all the expected refinancing issues, there will be ample possibilities to lock in new loans at high rates and favourable conditions.

1van der Spek, M. (2017). Investing in real estate debt: is it real estate or fixed income?. Abacus, 53(3), 349-370